Press Release

Germany's housing market remains under pressure, signs of relief for the new build segment

05 February 2026

Media Contact

Bettina Bierhalter

Ass. Director|Communications

- CBRE Time‑on‑Market Index*: Marketing periods for both rental and for‑sale apartments continued to shorten

- Building permits and new‑build activity rise slightly, though remain at a low level

- Median rents** are expected to rise by about five percent in 2025, reaching new highs in many locations

Germany’s housing market remained defined by a persistent structural imbalance throughout 2025. The gap between the available housing supply and actual demand did not narrow. The main driver continues to be chronic undersupply, amplified by high construction costs and ongoing restrictive lending conditions. This shortage is particularly pronounced in metropolitan regions, where limited availability and strong demand further intensify market pressure. Vacancy rates in many urban areas remain well below two percent, adding to market strain. By contrast, vacancy rates in some rural regions are significantly higher, making the supply gap primarily an issue for major cities and metropolitan areas.

“The limited housing supply continues to push rents upward. Many of the Top 20 cities reached new all time highs in 2025, while the volume of rental listings declined further,” says Stefan Wilke, Head of Residential Investment at CBRE in Germany. “The number of newly listed apartments remains at a historically low level.”

At the same time, there are signs of improvement in the new build segment. Compared with the previous year, new construction activity and issued building permits increased slightly. Expanded and improved housing construction incentives are creating cautious optimism among developers, but these measures have not yet produced a sustained market effect. These are the results of a recent study by the global real estate services provider CBRE, available on the company’s website.

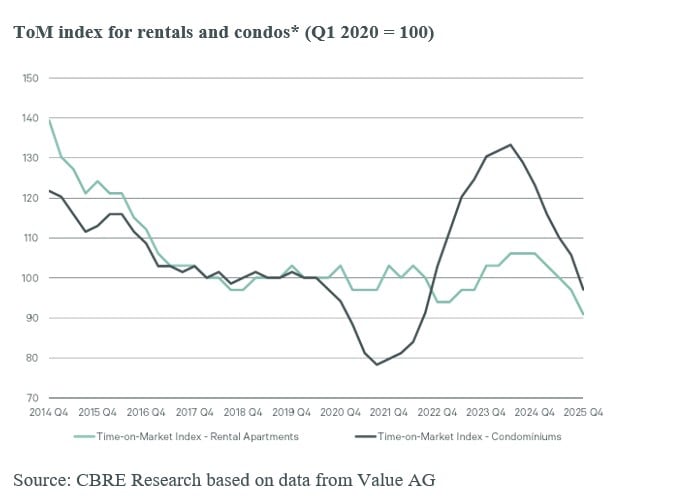

CBRE Time on Market Index shows shorter marketing periods

In both rental and owner occupied apartment segments, the average time properties remained listed on the market decreased in 2025. The Time on Market Index for rental listings has declined steadily since mid 2024 and reached a new low of 91 points in 2025. This corresponds to an average of 30 days nationwide, five days fewer than a year earlier. Marketing periods for condominiums also shortened, decreasing by 27 days to an average of 67 days by year end 2025.

Rents rose sharply again; purchase prices also increased slightly

Across the Top‑20 markets, median rents increased again by around five percent year‑on‑year, reaching new highs in many cities. The strongest rental growth in 2025 was recorded in Leipzig (+7.5%), Düsseldorf (+7.1%) and Dresden (+6.9%).

Asking prices for condominiums continued to stabilize in the Top 20 markets and even increased in several cities. Average prices in the Top 20 markets amounted to around €4,100 per sq m at the end of 2025, slightly above the previous year. The strongest price increases were observed in Essen (+8.8%), Bonn (+8.1%) and Dresden (+4.8%).

“Germany remains a rental driven market, as homeownership affordability continues to be limited by persistently high financing costs and substantial transaction related expenses,” says Jirka Stachen, Senior Director and Head of Research Consulting Continental Europe at CBRE. “At the same time, rapidly rising rents are increasingly pushing tenant cost burden ratios higher.”

Vacancy remains very low – regional differences persist

The ongoing rental momentum is supported by chronically low vacancy rates, particularly in metropolitan regions. In many major urban areas as well as southern and western agglomerations, vacancy rates are well below two percent.

“In growth markets and regions with strong in‑migration, supply constraints will continue to intensify given significant excess demand, further reducing vacancy rates,” says Michael Schlatterer, Managing Director Residential Valuation at CBRE in Germany. “In contrast, some rural regions in eastern Germany and several western transformation areas show vacancy rates above eight percent, largely due to demographic and structural factors.”

“We expect a broader recovery in residential construction following the latest political adjustments no earlier than 2027,” Wilke adds. “Rental growth is therefore likely to continue into 2026, with purchase prices rising moderately.”

* Methodology: The Time on Market Index indicates the normalized relative marketing duration of listed rental and for sale apartments. It measures the number of days between the listing date and the date the listing is removed. This does not necessarily mean the unit was actually rented or sold, but it provides reliable sentiment regarding the speed of marketing. The index is normalized to 100 at Q1 2020, enabling comparisons across product types. Relative changes between two points in time allow for temporal comparison.

** Note: Listed rents and asking prices are based on online apartment listings and do not represent actual in‑place rents or transaction prices.

- Building permits and new‑build activity rise slightly, though remain at a low level

- Median rents** are expected to rise by about five percent in 2025, reaching new highs in many locations

Germany’s housing market remained defined by a persistent structural imbalance throughout 2025. The gap between the available housing supply and actual demand did not narrow. The main driver continues to be chronic undersupply, amplified by high construction costs and ongoing restrictive lending conditions. This shortage is particularly pronounced in metropolitan regions, where limited availability and strong demand further intensify market pressure. Vacancy rates in many urban areas remain well below two percent, adding to market strain. By contrast, vacancy rates in some rural regions are significantly higher, making the supply gap primarily an issue for major cities and metropolitan areas.

“The limited housing supply continues to push rents upward. Many of the Top 20 cities reached new all time highs in 2025, while the volume of rental listings declined further,” says Stefan Wilke, Head of Residential Investment at CBRE in Germany. “The number of newly listed apartments remains at a historically low level.”

At the same time, there are signs of improvement in the new build segment. Compared with the previous year, new construction activity and issued building permits increased slightly. Expanded and improved housing construction incentives are creating cautious optimism among developers, but these measures have not yet produced a sustained market effect. These are the results of a recent study by the global real estate services provider CBRE, available on the company’s website.

CBRE Time on Market Index shows shorter marketing periods

In both rental and owner occupied apartment segments, the average time properties remained listed on the market decreased in 2025. The Time on Market Index for rental listings has declined steadily since mid 2024 and reached a new low of 91 points in 2025. This corresponds to an average of 30 days nationwide, five days fewer than a year earlier. Marketing periods for condominiums also shortened, decreasing by 27 days to an average of 67 days by year end 2025.

Rents rose sharply again; purchase prices also increased slightly

Across the Top‑20 markets, median rents increased again by around five percent year‑on‑year, reaching new highs in many cities. The strongest rental growth in 2025 was recorded in Leipzig (+7.5%), Düsseldorf (+7.1%) and Dresden (+6.9%).

Asking prices for condominiums continued to stabilize in the Top 20 markets and even increased in several cities. Average prices in the Top 20 markets amounted to around €4,100 per sq m at the end of 2025, slightly above the previous year. The strongest price increases were observed in Essen (+8.8%), Bonn (+8.1%) and Dresden (+4.8%).

“Germany remains a rental driven market, as homeownership affordability continues to be limited by persistently high financing costs and substantial transaction related expenses,” says Jirka Stachen, Senior Director and Head of Research Consulting Continental Europe at CBRE. “At the same time, rapidly rising rents are increasingly pushing tenant cost burden ratios higher.”

Vacancy remains very low – regional differences persist

The ongoing rental momentum is supported by chronically low vacancy rates, particularly in metropolitan regions. In many major urban areas as well as southern and western agglomerations, vacancy rates are well below two percent.

“In growth markets and regions with strong in‑migration, supply constraints will continue to intensify given significant excess demand, further reducing vacancy rates,” says Michael Schlatterer, Managing Director Residential Valuation at CBRE in Germany. “In contrast, some rural regions in eastern Germany and several western transformation areas show vacancy rates above eight percent, largely due to demographic and structural factors.”

“We expect a broader recovery in residential construction following the latest political adjustments no earlier than 2027,” Wilke adds. “Rental growth is therefore likely to continue into 2026, with purchase prices rising moderately.”

* Methodology: The Time on Market Index indicates the normalized relative marketing duration of listed rental and for sale apartments. It measures the number of days between the listing date and the date the listing is removed. This does not necessarily mean the unit was actually rented or sold, but it provides reliable sentiment regarding the speed of marketing. The index is normalized to 100 at Q1 2020, enabling comparisons across product types. Relative changes between two points in time allow for temporal comparison.

** Note: Listed rents and asking prices are based on online apartment listings and do not represent actual in‑place rents or transaction prices.

About CBRE Group, Inc

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services (based on 2025 revenue). The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, data center solutions); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services (based on 2025 revenue). The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, data center solutions); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.