Press Release

Germany’s industrial and logistics real estate market off to sound start to the year

21 April 2026

Media Contact

Ass. Director|Communications

- Take-up* drops two percent year-on-year to 1.3 million sqm in the first quarter of 2026

- Share of new builds in take-up sheds nine percentage points to 40 percent

- Prime yield up 4.1 percent as an average of the Top 5 markets

- Vacancy rate in the Big Box segment** down 0.3 percentage points to 4.7 percent since year-end 2025

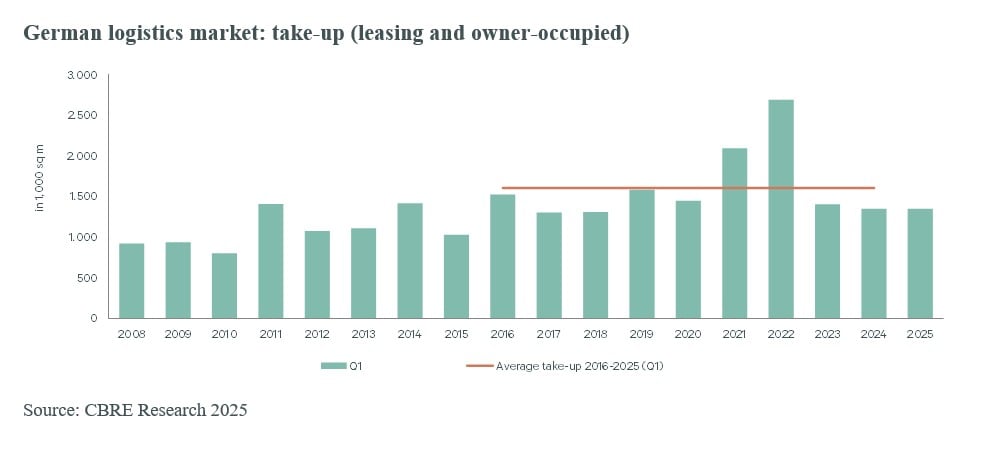

Germany’s investment market for industrial and logistics real estate delivered take-up of 1.3 million sqm in first quarter of 2026, reflecting a year-on-year decline of two percent. Take-up corresponded to the level posted by first quarters over the past three years Measured by take-up, Hamburg proved to be the strongest market, followed by the Ruhr region, with both markets exceeding the 100,000 sqm mark in the first quarter. This is the conclusion drawn in an analysis prepared by the global commercial real estate services company CBRE.

"While the general economic conditions are challenging, this is not reflected to the same degree across Germany’s industrial and logistics real estate market,” says Sarina Schekahn, Head of Industrial & Logistics Leasing at CBRE Germany. Big Box vacancy, for instance, has declined by 0.3 percentage points to 4.7 percent since the end of 2025, ultimately also because of the downtrend in speculative construction. Accordingly, take-up in new construction dropped 21 percent to 526,000 sqm compared with the first quarter of 2025. Prime rent expressed as an average of the Top 5 markets rose by 4.1 percent year on year to €9.21 per square meter also for this reason. Average rents presented a very disparate picture across the various logistics regions.

Aside from this, the Berlin market continued on its recovery trajectory, with take-up advancing to 82,000 sqm, accompanied by declining vacancies. A year ago, this logistics region was still struggling with a significant increase in vacancies. The logistics markets of Hamburg, Frankfurt/Rhine-Main and Munich have meanwhile been characterized more strongly again by shortage of space, which has never been fully resolved.

Demand from China holding steady

The demand from Chinese e-tailers and their allied logistics companies already observed back in 2025 also continued in the first quarter of 2026. The demand for space has now extended to regions outside North Rhine-Westphalia. In the first quarter, companies from China captured a share of 13 percent. “Whether production facilities of Chinese traders in Germany can be expected in the future due to the abolition of the duty-free privilege for small packages from China remains to be seen,” Schekahn comments.

Defense industry not a massive driver on the leasing market

In the first quarter of 2026, the most active segment in terms of demand proved to be that of transportation and logistics companies. This segment took a share of 41 percent in take-up, reflecting an increase of four percentage points above the level seen in the previous year’s quarter. Trading companies (including e-tailers) took second place with a share of 21 percent (down three percentage points), followed by production companies with 18 percent (down 14 percent).

“There are so far no signs of a massive defense-induced boom on the logistics leasing market as many companies mainly operate as owner-occupiers. This scenario could benefit suppliers, construction companies and built-to-suit property developers to a certain extent. At the same time, the defense sector, along with the Bundeswehr, is instrumental in stepping up the competition for premises,” explains Dr. Jan Linsin, Head of Research at CBRE Germany. Despite urgent demand for logistics space manifesting from the defense sector in the form of owner-occupiers, the industry’s share in take-up nevertheless declined. Consequently, the share of owner-occupiers came in at 12 percent in the first quarter (down 16 percentage points).

A further competitor for suitable land is constituted by data centers, above all in regions with an adequate power supply. “Data center developers generally have a cost advantage over logistics developers as higher square meter prices may be paid in the high margin data center market,” Linsin explains.

Outlook for the remainder of the year

“Germany’s industrial and logistics real estate market is in a structurally strong position while nevertheless remaining tied to economic developments in Germany. If economic growth turns out to be modest, as predicted at the last count, no significant developments in take-up can be expected,” Schekahn says in anticipation. “How – set apart from the economic trend in the logistics real estate market – the most recent geopolitical escalation in the Middle East plays out remains to be seen. The fuel crisis that will naturally have a huge impact on logistic companies’ operations could prove to be a constraint. By contrast, a commensurate upturn in the need for buffer storage could drive the demand for logistics space.”

* Outside the Top 5 markets CBRE only records deals of 5,000 sqm and over.

**Distribution hubs ≥ 10,000 m², built ≥ 2000, ceiling height ≥ 10 m

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services (based on 2025 revenue). The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, data center solutions); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.