Press Release

Gradual recovery on Germany’s real estate investment market firming up at the start of 2026

13 April 2026

Media Contact

Bettina Bierhalter

Ass. Director|Communications

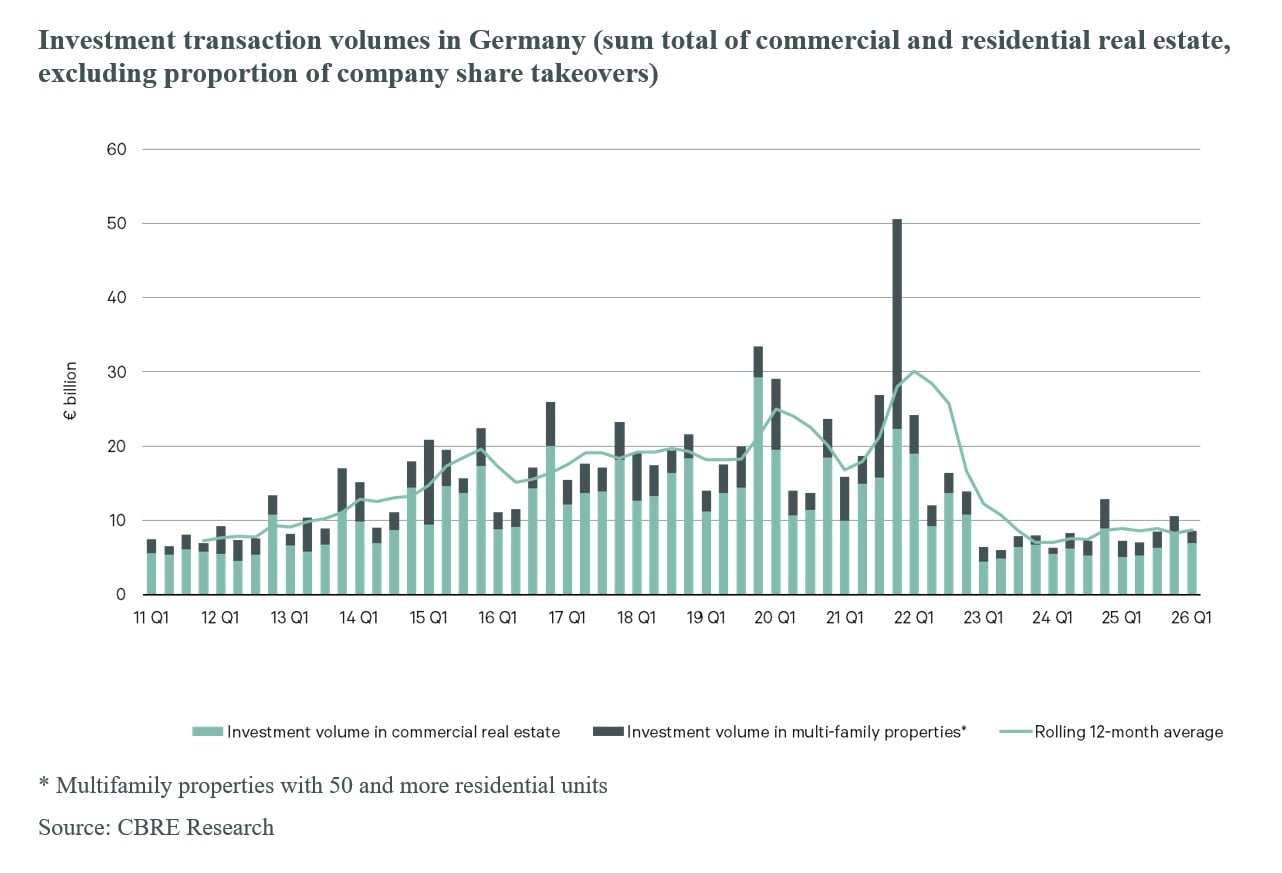

- The overall market exhibits a marked revival in the first quarter versus the year-earlier period (up 20 percent to €8.6 billion); moving 12-monthly average marks an increase of 4 percent

- Disparate development within the Top 7 locations

- Office real estate regains position as the strongest asset class

- Smaller single-asset deals driving market activity – structurally induced reticence in the case of large-scale deals

- Domestic investors dominate the market at the start of the year

- Yields largely stable compared with year-end 2025

Germany’s real estate transaction volume stood at around €8.6 billion in the first quarter of 2026, marking year-on-year growth of almost 20 percent. As against the exceptionally strong closing quarter of 2025, the volume nevertheless declined by some 19 percent essentially due to the pronounced year-end rally and a transaction momentum that is traditionally slower paced at the start of the year. These are the conclusions drawn in a current analysis prepared by the global commercial real estate services company CBRE.

“The investment market got off to a dynamic start in 2026, at least until the most recent geopolitical escalation in the Middle East. Although most of the transactions under way progressed, many players have become more cautious as regards new processes. The ‘cash flow is king’ imperative applies,” comments Marcus Lemli, Head of Investment at CBRE Germany. “What has become clear, however, is that people are getting somewhat more used to external geopolitical shocks. After all, real estate is still an investment with low volatility. This being the case, certainty, preserving value and stable rental income over the long term thanks to an active asset management approach are highly prized.” At 61 percent, the lion’s share of the investment volume was channeled into safe-haven oriented investments. Value-add captured 18 percent and opportunistic another 13 percent.

“Our underlying economic outlook indicates that the property sector fundamentals show stable, albeit more selective demand on the part of occupiers. At the same time, investors active on the real estate capital markets will be adopting a somewhat more reticent approach in view of the new inflation environment and generally heightened uncertainty,” explains Dr. Jan Linsin, Head of Research at CBRE Germany.

Office tops the league again

With a volume of some €2.1 billion, office real estate took its place as the strongest asset class in the market. The share of office in the overall volume came in at around 24 percent, reflecting growth of a good 60 percent compared with the first quarter of 2025. Consequently, office recorded not only the highest market share but also the strongest growth in absolute terms. Twelve of the 24 largest transactions above the €50 million mark were attributable to this asset class. With its purchase of a new building complex in Kaarst for the financial management operations of the Federal State of North Rhine-Westphalia, the public sector accounted for the largest office deal in the quarter. Aside from this, the OPES-Immobilien Group acquired the Alte Akademie in Munich from the Signa insolvency proceedings, thereby contributing to the transaction volume.

Office was followed by the residential segment that came in second place with around €1.7 billion, capturing a market share of approximately 19 percent. Despite the ongoing high volume, the result falls significantly short of the year-earlier figure. Industrial and logistics real estate ranked in third place with a transaction volume of some €1.4 billion, up 16 percent compared with the previous year’s quarter, thereby confirming stable demand.

Furthermore, healthcare properties achieved significant growth, delivering a volume of approximately €1.1 billion, boosted in particular by Aedifica’s pan-European majority takeover of Cofinimmo that, in relation to the portfolio acquired in Germany, was reflected in the high triple-digit million range. Development sites and other usage types also produced high growth rates while nevertheless remaining of secondary importance in terms of volume. By contrast, retail and hotel investments entered a downtrend.

Top 7 markets on the up

In the first quarter of 2026, the investment volume in Germany’s seven largest real estate markets totaled around €3 billion, which also marks growth of some 20 percent compared with the first quarter 2025. While the aggregated results indicate moderate stabilization, the Top 7 cities presented a markedly disparate picture. Berlin recorded a decline in volume that contrasts with the positive deviations in the other locations. The sale of the new ‘Deiker Höfe’ mixed-used property in Düsseldorf to HIH Invest enabled the city to achieve three times the investment volume compared with the first quarter of 2025, thus almost approximating the long-term average. Frankfurt staged a marked recovery compared with the previous year, which was also due to the sale of two buildings in the financial center’s banking quarter to companies from the banking and insurance sectors.

German investors particularly active

The market development in the first quarter of 2026 was driven primarily by domestic investors who realized a transaction volume of some €5.1 billion and stepped up their activities by around 26 percent year on year. Domestic buyers therefore took a share of almost 60 percent in the overall volume.

Foreign investors achieved a transaction volume that came in at around €3.5 billion, equivalent to an increase of some 12 percent compared with the first quarter of 2025. In quarter-on-quarter comparison, as well as in a longer term context, the exposure of international investors nevertheless fell short of the average although there are signs of a gradual improvement. “Germany remains one of the key target markets for many foreign investors’ real estate allocations, especially for players with a value-add approach,” Lemli comments. “Compared with some other European locations, however, specifically these investors consider the German market too expensive despite its size, liquidity and transparency, which is also evidenced by the ongoing high bid-ask spread.”

Price level stable for the time being

“In an environment of geopolitical challenges and the associated slowdown in economic recovery, inflation expectations on the rise, along with capital market and financing rates trending up, the market is on the verge of another potential recalibration of prices and thus of real estate yields,” Linsin says in anticipation.

Net initial yields have largely remained stable so far compared with year-end 2025. The most recent jump in oil prices has not had a direct impact on the real estate market but nevertheless exerts more pressure on the capital markets due to rising inflation expectations. In Germany, the currently elevated level of the yields of 10-year Bunds limits headroom for further yield compression. “The assumption for real estate yields is rather more for them to trend sideways or tick up moderately than for a rapid easing,” says Sandro Höselbarth, Head of Valuation & Advisory Services Germany at CBRE Germany. Usage types that are especially energy intensive and sensitive to interest rates are more vulnerable, as opposed to residential real estate that will remain comparatively stable due to its needs-driven demand. Against this backdrop, investors are increasingly focusing on income – stable cash flows, long-dated lease terms and defensive asset classes are becoming more important again.

Many single-asset transactions – but also large-scale deals – brought over the line

The transaction structure was clearly dominated by single-asset deals in the first quarter of 2026. Market activity was mostly driven by single-asset deals that generated a volume of around €6.2 billion, which reflects growth of around 28 percent compared with the previous year’s period. Ten large-scale single-asset deals concluded in the various asset classes also contributed to this result, especially in the office real estate segment, as well as in residential, logistics and retail. By far the largest single-asset transaction of around €400 million took place outside the top markets, namely the aforementioned acquisition by the Federal State of North Rhine-Westphalia’s Ministry of Finance.

By contrast, the segment of portfolio acquisitions that came in at approximately €2.5 billion proved to be relatively weak although several large portfolio deals were concluded – along with two deals in the healthcare property sector, one in each of the segments of logistics, leisure, retail and office.

Large-scale transactions in excess of €100 million increased in terms of volume and numbers versus the first quarter of 2025 without, however, repeating the level of earlier years. The first three months of 2026 saw 16 deals transacted in this dimension in an aggregated amount of just shy of €3.6 billion. Of this volume, five were attributable to portfolio sales and ten to single-asset transactions, with 14 to commercial real estate and two to residential investment. “Large-scale investments continue to be dominated by extreme selectivity and a limited supply of marketable property,” Lemli states.

The market experienced a significant upswing in the smaller scale segment in particular. Transactions below the ten-million-euro mark recorded significant year-on-year growth, partly achieving or even exceeding their long-term average. The mid range in categories between €10 million and €50 million developed moderately well. Accordingly, the average volume per deal shed 10 percent to just under €22 million following on from a good €24 million in the first quarter of 2025 and is currently running around one fifth below the five-year average for the first quarters. All in all, just under 100 transactions equivalent to one third more were registered compared with the previous year’s quarter.

Outlook for the remainder of the year

“We assume that the market will pick up momentum on the back of a greater supply of property. Open-ended real estate funds will continue and even step up their efforts to streamline their portfolios. At the same time, banks will also be putting properties on the market as German banks’ NLP ratio in real estate lending is at its highest in a European comparison,” Lemli explains.

- Disparate development within the Top 7 locations

- Office real estate regains position as the strongest asset class

- Smaller single-asset deals driving market activity – structurally induced reticence in the case of large-scale deals

- Domestic investors dominate the market at the start of the year

- Yields largely stable compared with year-end 2025

Germany’s real estate transaction volume stood at around €8.6 billion in the first quarter of 2026, marking year-on-year growth of almost 20 percent. As against the exceptionally strong closing quarter of 2025, the volume nevertheless declined by some 19 percent essentially due to the pronounced year-end rally and a transaction momentum that is traditionally slower paced at the start of the year. These are the conclusions drawn in a current analysis prepared by the global commercial real estate services company CBRE.

“The investment market got off to a dynamic start in 2026, at least until the most recent geopolitical escalation in the Middle East. Although most of the transactions under way progressed, many players have become more cautious as regards new processes. The ‘cash flow is king’ imperative applies,” comments Marcus Lemli, Head of Investment at CBRE Germany. “What has become clear, however, is that people are getting somewhat more used to external geopolitical shocks. After all, real estate is still an investment with low volatility. This being the case, certainty, preserving value and stable rental income over the long term thanks to an active asset management approach are highly prized.” At 61 percent, the lion’s share of the investment volume was channeled into safe-haven oriented investments. Value-add captured 18 percent and opportunistic another 13 percent.

“Our underlying economic outlook indicates that the property sector fundamentals show stable, albeit more selective demand on the part of occupiers. At the same time, investors active on the real estate capital markets will be adopting a somewhat more reticent approach in view of the new inflation environment and generally heightened uncertainty,” explains Dr. Jan Linsin, Head of Research at CBRE Germany.

Office tops the league again

With a volume of some €2.1 billion, office real estate took its place as the strongest asset class in the market. The share of office in the overall volume came in at around 24 percent, reflecting growth of a good 60 percent compared with the first quarter of 2025. Consequently, office recorded not only the highest market share but also the strongest growth in absolute terms. Twelve of the 24 largest transactions above the €50 million mark were attributable to this asset class. With its purchase of a new building complex in Kaarst for the financial management operations of the Federal State of North Rhine-Westphalia, the public sector accounted for the largest office deal in the quarter. Aside from this, the OPES-Immobilien Group acquired the Alte Akademie in Munich from the Signa insolvency proceedings, thereby contributing to the transaction volume.

Office was followed by the residential segment that came in second place with around €1.7 billion, capturing a market share of approximately 19 percent. Despite the ongoing high volume, the result falls significantly short of the year-earlier figure. Industrial and logistics real estate ranked in third place with a transaction volume of some €1.4 billion, up 16 percent compared with the previous year’s quarter, thereby confirming stable demand.

Furthermore, healthcare properties achieved significant growth, delivering a volume of approximately €1.1 billion, boosted in particular by Aedifica’s pan-European majority takeover of Cofinimmo that, in relation to the portfolio acquired in Germany, was reflected in the high triple-digit million range. Development sites and other usage types also produced high growth rates while nevertheless remaining of secondary importance in terms of volume. By contrast, retail and hotel investments entered a downtrend.

Top 7 markets on the up

In the first quarter of 2026, the investment volume in Germany’s seven largest real estate markets totaled around €3 billion, which also marks growth of some 20 percent compared with the first quarter 2025. While the aggregated results indicate moderate stabilization, the Top 7 cities presented a markedly disparate picture. Berlin recorded a decline in volume that contrasts with the positive deviations in the other locations. The sale of the new ‘Deiker Höfe’ mixed-used property in Düsseldorf to HIH Invest enabled the city to achieve three times the investment volume compared with the first quarter of 2025, thus almost approximating the long-term average. Frankfurt staged a marked recovery compared with the previous year, which was also due to the sale of two buildings in the financial center’s banking quarter to companies from the banking and insurance sectors.

German investors particularly active

The market development in the first quarter of 2026 was driven primarily by domestic investors who realized a transaction volume of some €5.1 billion and stepped up their activities by around 26 percent year on year. Domestic buyers therefore took a share of almost 60 percent in the overall volume.

Foreign investors achieved a transaction volume that came in at around €3.5 billion, equivalent to an increase of some 12 percent compared with the first quarter of 2025. In quarter-on-quarter comparison, as well as in a longer term context, the exposure of international investors nevertheless fell short of the average although there are signs of a gradual improvement. “Germany remains one of the key target markets for many foreign investors’ real estate allocations, especially for players with a value-add approach,” Lemli comments. “Compared with some other European locations, however, specifically these investors consider the German market too expensive despite its size, liquidity and transparency, which is also evidenced by the ongoing high bid-ask spread.”

Price level stable for the time being

“In an environment of geopolitical challenges and the associated slowdown in economic recovery, inflation expectations on the rise, along with capital market and financing rates trending up, the market is on the verge of another potential recalibration of prices and thus of real estate yields,” Linsin says in anticipation.

Net initial yields have largely remained stable so far compared with year-end 2025. The most recent jump in oil prices has not had a direct impact on the real estate market but nevertheless exerts more pressure on the capital markets due to rising inflation expectations. In Germany, the currently elevated level of the yields of 10-year Bunds limits headroom for further yield compression. “The assumption for real estate yields is rather more for them to trend sideways or tick up moderately than for a rapid easing,” says Sandro Höselbarth, Head of Valuation & Advisory Services Germany at CBRE Germany. Usage types that are especially energy intensive and sensitive to interest rates are more vulnerable, as opposed to residential real estate that will remain comparatively stable due to its needs-driven demand. Against this backdrop, investors are increasingly focusing on income – stable cash flows, long-dated lease terms and defensive asset classes are becoming more important again.

Many single-asset transactions – but also large-scale deals – brought over the line

The transaction structure was clearly dominated by single-asset deals in the first quarter of 2026. Market activity was mostly driven by single-asset deals that generated a volume of around €6.2 billion, which reflects growth of around 28 percent compared with the previous year’s period. Ten large-scale single-asset deals concluded in the various asset classes also contributed to this result, especially in the office real estate segment, as well as in residential, logistics and retail. By far the largest single-asset transaction of around €400 million took place outside the top markets, namely the aforementioned acquisition by the Federal State of North Rhine-Westphalia’s Ministry of Finance.

By contrast, the segment of portfolio acquisitions that came in at approximately €2.5 billion proved to be relatively weak although several large portfolio deals were concluded – along with two deals in the healthcare property sector, one in each of the segments of logistics, leisure, retail and office.

Large-scale transactions in excess of €100 million increased in terms of volume and numbers versus the first quarter of 2025 without, however, repeating the level of earlier years. The first three months of 2026 saw 16 deals transacted in this dimension in an aggregated amount of just shy of €3.6 billion. Of this volume, five were attributable to portfolio sales and ten to single-asset transactions, with 14 to commercial real estate and two to residential investment. “Large-scale investments continue to be dominated by extreme selectivity and a limited supply of marketable property,” Lemli states.

The market experienced a significant upswing in the smaller scale segment in particular. Transactions below the ten-million-euro mark recorded significant year-on-year growth, partly achieving or even exceeding their long-term average. The mid range in categories between €10 million and €50 million developed moderately well. Accordingly, the average volume per deal shed 10 percent to just under €22 million following on from a good €24 million in the first quarter of 2025 and is currently running around one fifth below the five-year average for the first quarters. All in all, just under 100 transactions equivalent to one third more were registered compared with the previous year’s quarter.

Outlook for the remainder of the year

“We assume that the market will pick up momentum on the back of a greater supply of property. Open-ended real estate funds will continue and even step up their efforts to streamline their portfolios. At the same time, banks will also be putting properties on the market as German banks’ NLP ratio in real estate lending is at its highest in a European comparison,” Lemli explains.

About CBRE Group, Inc

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services (based on 2025 revenue). The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, data center solutions); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services (based on 2025 revenue). The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, data center solutions); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.