Press Release

Retail real estate investment market: grocery-anchored retail properties as a cornerstone of stability at the start of the year – keener interest in shopping centers

14 April 2026

Media Contact

Bettina Bierhalter

Ass. Director|Communications

- Investment volume drops 13 percent to €1.1 billion compared with the first quarter of 2025

- Focus on grocery-anchored properties – but shopping centers also of interest

- Stable prime yields

Germany’s retail real estate investment market delivered a transaction volume of €1.1 billion in the first quarter of 2026, reflecting a decline of 13 percent compared with the previous year’s period. A larger share of 23 percent (up five percentage points) has advanced the relative importance of the Top 7 markets. This is the conclusion drawn in an analysis prepared by the global commercial real estate services company CBRE.

“Germany’s retail real estate investment market experienced a sound opening quarter,” says Jan Schönherr, Head of Retail Investment at CBRE. Market activity was characterized by a comparatively high number of transactions (75) that nevertheless generated a significantly smaller purchase price volume on average than a year ago. The share of portfolios also shed 11 percentage points to 24 percent in a year-on-year comparison. Larger deals in excess of €100 million have so far remained the exception. Among other transactions, this also included the sale of the Powerfood portfolio as well as that of a majority holding in Leipzig’s Höfe am Brühl shopping center. “This transaction shows that large-scale shopping centers also most definitely appeal to prospective investors, which applies first and foremost to international investors who are especially interested in value-add and core-plus properties,” Schönherr explains. By contrast, German investors concentrated mainly on core properties.

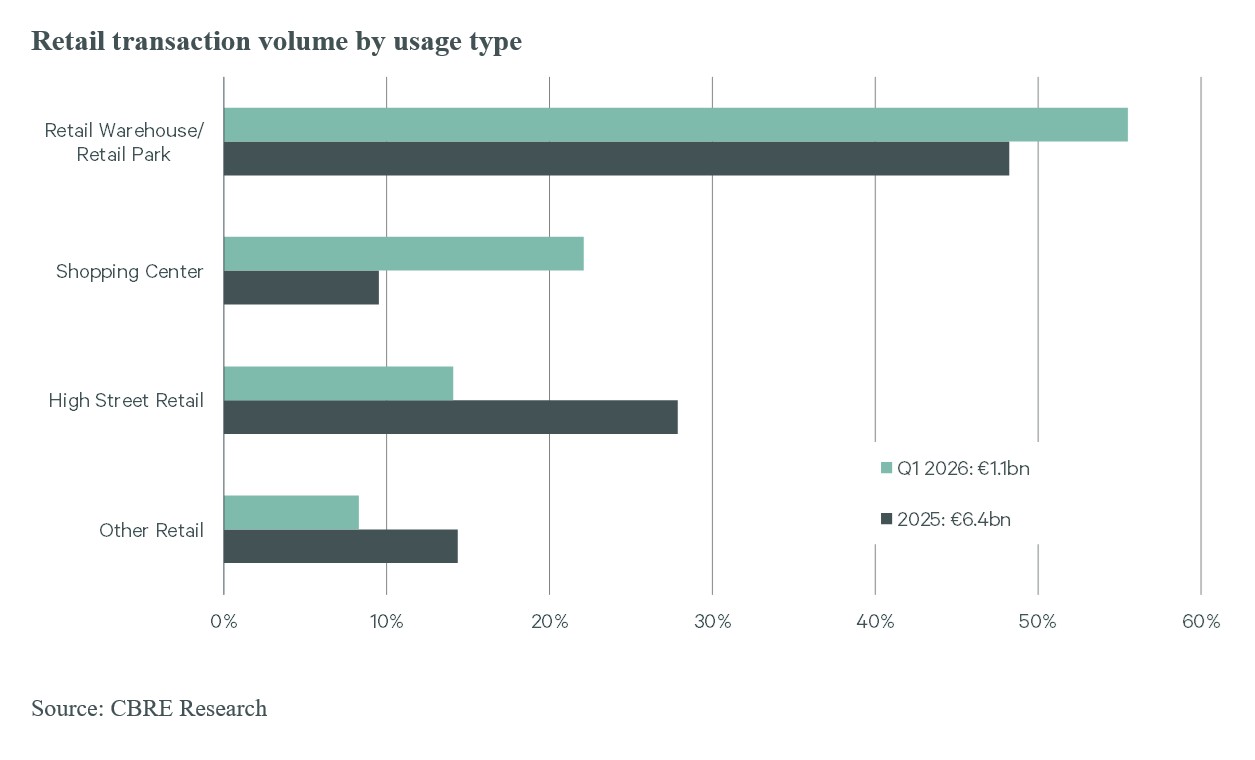

“In the current phase that is determined by geopolitical upheavals and growing concerns about inflation, interest in grocery-anchored retail properties with long-dated lease agreements generating relatively stable cash flows is on the rise,” Schönherr comments. Local shopping facilities and food discounters resonate with current consumer sentiment and, from an investor standpoint, offer a suitable, defensive investment product. The segment of retail warehouses and retail parks captured the lion’s share in the transaction volume, accounting for more than half the entire investment volume with a share of 56 percent (Q1 2025: 53 percent). Shopping centers followed on in second place with 22 percent (Q1 2025: three percent), followed by high street properties with 14 percent (Q1 2025: 15 percent). Shopping centers are increasingly attracting investors whose aim is to reposition these properties by applying mixed-use concepts.

“At the last count, purchase price returns remained stable across all sub-segments of the retail property market,” comments Anne Gimpel, Team Leader Valuation Advisory Services at CBRE. A few slight changes only come to light in comparison with the first quarter of 2025: the prime yields of high street properties in the Top 7 cities shed 0.2 percentage points to 4.44 percent, for instance. At the same time, shopping center prime yields in secondary locations climbed 0.25 percentage points to 7.75 percent. Shopping centers in prime locations remained stable at 5.9 percent. Similarly, no changes took place in the prime yields of food markets (4.6 percent) and retail parks (4.9 percent).

Against the backdrop of geopolitical tensions, a faltering economic recovery, and rising expectations of inflation, along with higher capital market and financing costs, a potential adjustment to the price level is on the cards, with the corresponding impact on the development of property yields.

Financing capability permeating transaction momentum

The sustained global crises, especially rising energy costs and ongoing disruptions to supply chains, are fanning fresh fears about inflation. Irrespective of further possible interest rate moves, financing capability has already been notably constrained: A determining factor here includes the higher spread compared with another increase in the yield on 10-year Bunds, paired with persistently high construction costs. Consequently, the market position of equity investors has firmed up as opposed to leveraged strategies that are only adopted on a selective basis. As equity investors naturally allocate limited volumes, large-scale, highly leveraged portfolio transactions remain the exception.

Outlook for the remainder of the year

“There are a number of larger properties in the transaction pipeline that will contribute to a revival in the market over the course of the year,” Schönherr says in anticipation. “This concerns various transactions at the level of both single assets and portfolios, which includes high street properties, as well as grocery-anchored properties and shopping centers.

- Focus on grocery-anchored properties – but shopping centers also of interest

- Stable prime yields

Germany’s retail real estate investment market delivered a transaction volume of €1.1 billion in the first quarter of 2026, reflecting a decline of 13 percent compared with the previous year’s period. A larger share of 23 percent (up five percentage points) has advanced the relative importance of the Top 7 markets. This is the conclusion drawn in an analysis prepared by the global commercial real estate services company CBRE.

“Germany’s retail real estate investment market experienced a sound opening quarter,” says Jan Schönherr, Head of Retail Investment at CBRE. Market activity was characterized by a comparatively high number of transactions (75) that nevertheless generated a significantly smaller purchase price volume on average than a year ago. The share of portfolios also shed 11 percentage points to 24 percent in a year-on-year comparison. Larger deals in excess of €100 million have so far remained the exception. Among other transactions, this also included the sale of the Powerfood portfolio as well as that of a majority holding in Leipzig’s Höfe am Brühl shopping center. “This transaction shows that large-scale shopping centers also most definitely appeal to prospective investors, which applies first and foremost to international investors who are especially interested in value-add and core-plus properties,” Schönherr explains. By contrast, German investors concentrated mainly on core properties.

“In the current phase that is determined by geopolitical upheavals and growing concerns about inflation, interest in grocery-anchored retail properties with long-dated lease agreements generating relatively stable cash flows is on the rise,” Schönherr comments. Local shopping facilities and food discounters resonate with current consumer sentiment and, from an investor standpoint, offer a suitable, defensive investment product. The segment of retail warehouses and retail parks captured the lion’s share in the transaction volume, accounting for more than half the entire investment volume with a share of 56 percent (Q1 2025: 53 percent). Shopping centers followed on in second place with 22 percent (Q1 2025: three percent), followed by high street properties with 14 percent (Q1 2025: 15 percent). Shopping centers are increasingly attracting investors whose aim is to reposition these properties by applying mixed-use concepts.

“At the last count, purchase price returns remained stable across all sub-segments of the retail property market,” comments Anne Gimpel, Team Leader Valuation Advisory Services at CBRE. A few slight changes only come to light in comparison with the first quarter of 2025: the prime yields of high street properties in the Top 7 cities shed 0.2 percentage points to 4.44 percent, for instance. At the same time, shopping center prime yields in secondary locations climbed 0.25 percentage points to 7.75 percent. Shopping centers in prime locations remained stable at 5.9 percent. Similarly, no changes took place in the prime yields of food markets (4.6 percent) and retail parks (4.9 percent).

Against the backdrop of geopolitical tensions, a faltering economic recovery, and rising expectations of inflation, along with higher capital market and financing costs, a potential adjustment to the price level is on the cards, with the corresponding impact on the development of property yields.

Financing capability permeating transaction momentum

The sustained global crises, especially rising energy costs and ongoing disruptions to supply chains, are fanning fresh fears about inflation. Irrespective of further possible interest rate moves, financing capability has already been notably constrained: A determining factor here includes the higher spread compared with another increase in the yield on 10-year Bunds, paired with persistently high construction costs. Consequently, the market position of equity investors has firmed up as opposed to leveraged strategies that are only adopted on a selective basis. As equity investors naturally allocate limited volumes, large-scale, highly leveraged portfolio transactions remain the exception.

Outlook for the remainder of the year

“There are a number of larger properties in the transaction pipeline that will contribute to a revival in the market over the course of the year,” Schönherr says in anticipation. “This concerns various transactions at the level of both single assets and portfolios, which includes high street properties, as well as grocery-anchored properties and shopping centers.

About CBRE Group, Inc

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services (based on 2025 revenue). The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, data center solutions); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services (based on 2025 revenue). The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, data center solutions); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.