Press Release

Ongoing differentiation based on location and property quality driving prime and average rents in the Top 5 office leasing markets

13 January 2026

Media Contact

Bettina Bierhalter

Ass. Director|Communications

- Rising prime and average rents highlight occupier sensitivity to quality

- Office take-up at 2.23 million sq m in the Top 5 markets in 2025, down slightly compared to the previous year

- Vacancies on the up in decentral locations and in outdated properties lacking energy efficiency

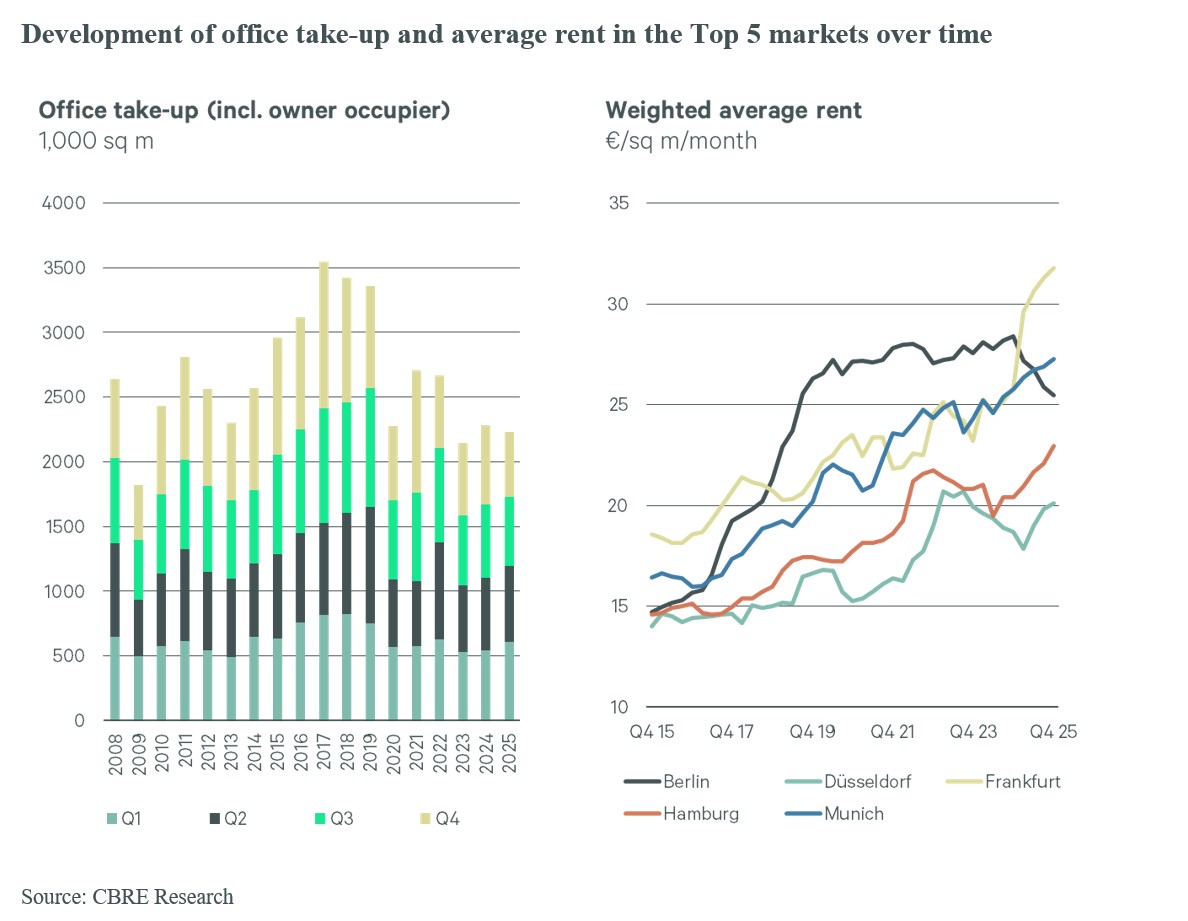

Office take-up in Germany’s Top 5 office markets came in at 2.23 million sq m in 2025, signaling a marginal decline of two percent compared to 2024. The market has therefore settled seven percent below the average take-up of the last five years (2020-2024). Overall performance was supported by very brisk demand for contemporary new office space in Frankfurt (up 60 percent). Other locations sustained declines between eight and 19 percent. Munich with a volume of 557,500 sq m nevertheless slightly exceeded that of Frankfurt. These are the conclusions drawn from current analysis prepared by the global commercial real estate services company CBRE.

“The market environment remained very challenging in 2025, characterized by a great deal of uncertainty, with a commensurate impact on location- and leasing-related decisions. Furthermore, the availability of the right office space in central locations is quite simply lacking.”

Carsten Ape, Head of Office Leasing Germany at CBRE

Rental growth across the board

The dearth of high quality office space in good locations has sent rents up considerably. As a result, achievable prime rent as an average of the Top 5 locations rose across the board. The following cities proved to be particularly dynamic: Hamburg (up 13.9 percent to €41.00 per sq m and month) and Frankfurt (up 12.2 percent to €55.00). A new psychological milestone of €60.00 was also reached in Munich.

“This increase at the top end of the market shows that prime office space in the top locations that satisfies the highest ESG requirements has disengaged from the general market decline and is enjoying sustained demand from a range of occupiers.”

Dr. Jan Linsin, Head of Research at CBRE Germany

Divergence in the market is even more pronounced as reflected by the weighted average rent that, expressed as an average of the Top 5, increased by just under eight percent to €26.68 per sq m and month. Frankfurt stands out here again with growth of more than 23 percent (€31.79) that, in addition to large-volume lettings in banking locations, is also attributable to leases concluded at maximum rent in planned new buildings. Hamburg (up 12.4 percent) and Düsseldorf (up 7.5 percent) also recorded significant growth based on leases in project developments. The average rent in Munich advanced substantially by 5.8 percent.

Berlin was the only exception: While prime rent remained virtually stable (up 1.1 percent), average rent shed 10.3 percent to €25.47 in a year-on-year comparison. This development in Germany’s capital city is mainly explained by the differentiation based on location and property quality that has triggered further drastic price adjustments.

“This split in the market is clear evidence of a structural flight to quality that, against the backdrop of rising average rents, mainly reflects great willingness to pay for ESG-compliant CBD properties. While the premium segment is breaking records, occupiers optimizing their office space in conjunction with quality requirements is exerting growing price pressure on decentralized existing stock,” Ape says.

Small-scale meets with major deals

“The uncertain economic situation has resulted in a risk averse approach to rent,” Linsin comments. This is borne out by major occupiers renewing leases (10,000 sq m and more), a figure that has risen by 79 percent compared to 2024.

Reticence and a focus on optimizing existing stock determine the deal structures of the individual locations, albeit in ways that vary greatly. In Berlin, this trend manifested in pronounced small-scale segmentation – in a year-on-year comparison, the office market recorded the weakest development in take-up while nevertheless proving particularly dynamic in the small-unit segment. While the number of leases concluded climbed by 22 percent during 2025 as a whole, the average deal size virtually halved. A much more stable picture was presented by the markets in Hamburg, Munich and Düsseldorf in the mid-range segment. In these locations, the majority of take-ups with a share of 22 percent was accounted for by the size category between 1,000 and 2,500 sq m, which vouches for the ongoing demand of SMEs for a more efficient office floor space. By contrast, Frankfurt am Main recorded record take-up that was driven almost exclusively by the large-scale leasing segment. Major occupiers such as Commerzbank, ING and KPMG forged ahead with their strategic realignments, most especially in the highly sought-after banking locations and in new buildings being developed in selected city fringe locations. Consequently, the size category above 10,000 sq m that also captured 22 percent of take-up functioned as a key market driver here.

Owing to the size of the deals, the accumulated sectoral share of consultants and banks in the Top 5 markets, combined with financial service providers, came in at 23 percent, followed by the sectors of industry, construction (14 percent), real estate (nine percent) and IT (eight percent) that, given the already high density of tech companies and digital start-ups, captured the largest share in Berlin.

Right location lacking supply

The cyclical increase in supply in the Top 5 cities continued in the fourth quarter of 2025. Office supply (defined as vacancy, available subleased space and speculative completions in the next twelve months) rose by 11 percent to eight million sq m compared with 2024. The vacancy rate in the Top 5 stood at 8.4 percent at the end of the year, 1.1 percentage points above the year-earlier figure. While structural vacancy in decentralized locations and energetically obsolete properties increased at a disproportionate rate, vacancy rates in the central locations (CBDs) were considerably lower at a mere 6.6 percent, with extremely limited availability. “This divergence highlights the trend indicating that properties not conforming to the latest ESG criteria or in decentralized locations with poor local public transport connections are missing out as on market activity,” Linsin says. The situation is exacerbated by developments in the new construction segment: After four years, the completion volume in 2025 dropped below the mark of one million sq m, declining by 14 percent compared to the year before. “The decline in new buildings has resulted in the extremely rare availability of prime office space despite the general increase in supply, which has further intensified the competition between occupiers for high quality office space in city centers,” Ape states.

Outlook for 2026

Future demand for office space will be increasingly determined by strategic considerations that far exceed the pure square meter price. Office has firmly established itself as a physical anchor point for corporate culture, collaboration and team cohesiveness and is increasingly viewed by companies as more of a productivity factor rather than a cost factor. In a market environment characterized by hybrid working models, the location and fit-out are becoming key factors for winning and retaining employees in the long term. “This repositioning as a strategic asset is fueling the demand for premium quality and best locations,” Linsin explains.

However, demand focused on quality is set coincide with supply dwindling drastically in the coming years. Construction activity continues to record significant declines: In terms of the pipeline, new office space totaling around 3.7 million sq m in the Top 5 markets will be added in the next three years. “What appears to be substantial at first glance turns out to be a historical shortfall on closer analysis,” Ape comments. Comparison with the previous year’s forecast shows a decline of 10 percent and, as against the forecast for the last five years, the volume has slumped by as much as 35 percent. Moreover, there is a marked geographical discrepancy between supply and demand. Although around 59 percent of the office space planned over the next three years is still available on a speculative basis, two thirds of this volume are located in city fringe submarkets. Fresh supply in the extremely desirable central CBD locations is, however, becoming an increasingly scarce commodity.

Despite the restrictive pipeline, there are indications of stabilization in the domain of project implementation. A positive signal emanates from the significant drop in projects where construction has been halted. While, in 2024, 19 projects were put on ice, a current analysis only counts seven projects in which building work has been suspended. “A sustainable market recovery will be mainly defined by the intrinsic value of office space and its future viability. Swift absorption of available office space can be expected in the desirable central office locations due to quality-oriented demand and the declining volume of new buildings.

- Office take-up at 2.23 million sq m in the Top 5 markets in 2025, down slightly compared to the previous year

- Vacancies on the up in decentral locations and in outdated properties lacking energy efficiency

Office take-up in Germany’s Top 5 office markets came in at 2.23 million sq m in 2025, signaling a marginal decline of two percent compared to 2024. The market has therefore settled seven percent below the average take-up of the last five years (2020-2024). Overall performance was supported by very brisk demand for contemporary new office space in Frankfurt (up 60 percent). Other locations sustained declines between eight and 19 percent. Munich with a volume of 557,500 sq m nevertheless slightly exceeded that of Frankfurt. These are the conclusions drawn from current analysis prepared by the global commercial real estate services company CBRE.

“The market environment remained very challenging in 2025, characterized by a great deal of uncertainty, with a commensurate impact on location- and leasing-related decisions. Furthermore, the availability of the right office space in central locations is quite simply lacking.”

Carsten Ape, Head of Office Leasing Germany at CBRE

Rental growth across the board

The dearth of high quality office space in good locations has sent rents up considerably. As a result, achievable prime rent as an average of the Top 5 locations rose across the board. The following cities proved to be particularly dynamic: Hamburg (up 13.9 percent to €41.00 per sq m and month) and Frankfurt (up 12.2 percent to €55.00). A new psychological milestone of €60.00 was also reached in Munich.

“This increase at the top end of the market shows that prime office space in the top locations that satisfies the highest ESG requirements has disengaged from the general market decline and is enjoying sustained demand from a range of occupiers.”

Dr. Jan Linsin, Head of Research at CBRE Germany

Divergence in the market is even more pronounced as reflected by the weighted average rent that, expressed as an average of the Top 5, increased by just under eight percent to €26.68 per sq m and month. Frankfurt stands out here again with growth of more than 23 percent (€31.79) that, in addition to large-volume lettings in banking locations, is also attributable to leases concluded at maximum rent in planned new buildings. Hamburg (up 12.4 percent) and Düsseldorf (up 7.5 percent) also recorded significant growth based on leases in project developments. The average rent in Munich advanced substantially by 5.8 percent.

Berlin was the only exception: While prime rent remained virtually stable (up 1.1 percent), average rent shed 10.3 percent to €25.47 in a year-on-year comparison. This development in Germany’s capital city is mainly explained by the differentiation based on location and property quality that has triggered further drastic price adjustments.

“This split in the market is clear evidence of a structural flight to quality that, against the backdrop of rising average rents, mainly reflects great willingness to pay for ESG-compliant CBD properties. While the premium segment is breaking records, occupiers optimizing their office space in conjunction with quality requirements is exerting growing price pressure on decentralized existing stock,” Ape says.

Small-scale meets with major deals

“The uncertain economic situation has resulted in a risk averse approach to rent,” Linsin comments. This is borne out by major occupiers renewing leases (10,000 sq m and more), a figure that has risen by 79 percent compared to 2024.

Reticence and a focus on optimizing existing stock determine the deal structures of the individual locations, albeit in ways that vary greatly. In Berlin, this trend manifested in pronounced small-scale segmentation – in a year-on-year comparison, the office market recorded the weakest development in take-up while nevertheless proving particularly dynamic in the small-unit segment. While the number of leases concluded climbed by 22 percent during 2025 as a whole, the average deal size virtually halved. A much more stable picture was presented by the markets in Hamburg, Munich and Düsseldorf in the mid-range segment. In these locations, the majority of take-ups with a share of 22 percent was accounted for by the size category between 1,000 and 2,500 sq m, which vouches for the ongoing demand of SMEs for a more efficient office floor space. By contrast, Frankfurt am Main recorded record take-up that was driven almost exclusively by the large-scale leasing segment. Major occupiers such as Commerzbank, ING and KPMG forged ahead with their strategic realignments, most especially in the highly sought-after banking locations and in new buildings being developed in selected city fringe locations. Consequently, the size category above 10,000 sq m that also captured 22 percent of take-up functioned as a key market driver here.

Owing to the size of the deals, the accumulated sectoral share of consultants and banks in the Top 5 markets, combined with financial service providers, came in at 23 percent, followed by the sectors of industry, construction (14 percent), real estate (nine percent) and IT (eight percent) that, given the already high density of tech companies and digital start-ups, captured the largest share in Berlin.

Right location lacking supply

The cyclical increase in supply in the Top 5 cities continued in the fourth quarter of 2025. Office supply (defined as vacancy, available subleased space and speculative completions in the next twelve months) rose by 11 percent to eight million sq m compared with 2024. The vacancy rate in the Top 5 stood at 8.4 percent at the end of the year, 1.1 percentage points above the year-earlier figure. While structural vacancy in decentralized locations and energetically obsolete properties increased at a disproportionate rate, vacancy rates in the central locations (CBDs) were considerably lower at a mere 6.6 percent, with extremely limited availability. “This divergence highlights the trend indicating that properties not conforming to the latest ESG criteria or in decentralized locations with poor local public transport connections are missing out as on market activity,” Linsin says. The situation is exacerbated by developments in the new construction segment: After four years, the completion volume in 2025 dropped below the mark of one million sq m, declining by 14 percent compared to the year before. “The decline in new buildings has resulted in the extremely rare availability of prime office space despite the general increase in supply, which has further intensified the competition between occupiers for high quality office space in city centers,” Ape states.

Outlook for 2026

Future demand for office space will be increasingly determined by strategic considerations that far exceed the pure square meter price. Office has firmly established itself as a physical anchor point for corporate culture, collaboration and team cohesiveness and is increasingly viewed by companies as more of a productivity factor rather than a cost factor. In a market environment characterized by hybrid working models, the location and fit-out are becoming key factors for winning and retaining employees in the long term. “This repositioning as a strategic asset is fueling the demand for premium quality and best locations,” Linsin explains.

However, demand focused on quality is set coincide with supply dwindling drastically in the coming years. Construction activity continues to record significant declines: In terms of the pipeline, new office space totaling around 3.7 million sq m in the Top 5 markets will be added in the next three years. “What appears to be substantial at first glance turns out to be a historical shortfall on closer analysis,” Ape comments. Comparison with the previous year’s forecast shows a decline of 10 percent and, as against the forecast for the last five years, the volume has slumped by as much as 35 percent. Moreover, there is a marked geographical discrepancy between supply and demand. Although around 59 percent of the office space planned over the next three years is still available on a speculative basis, two thirds of this volume are located in city fringe submarkets. Fresh supply in the extremely desirable central CBD locations is, however, becoming an increasingly scarce commodity.

Despite the restrictive pipeline, there are indications of stabilization in the domain of project implementation. A positive signal emanates from the significant drop in projects where construction has been halted. While, in 2024, 19 projects were put on ice, a current analysis only counts seven projects in which building work has been suspended. “A sustainable market recovery will be mainly defined by the intrinsic value of office space and its future viability. Swift absorption of available office space can be expected in the desirable central office locations due to quality-oriented demand and the declining volume of new buildings.

About CBRE Group, Inc

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services (based on 2025 revenue). The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, data center solutions); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services (based on 2025 revenue). The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, data center solutions); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.