Press Release

Real estate investment market on the up in the first half of 2026

08 July 2026

Media Contact

Ass. Director|Communications

- Office investment posts notable growth, with logistics and industry also contributing to the upturn

- Top 7 locations continued to gain importance

- Pricing process at an advanced stage – pressure to sell widening the range of available product

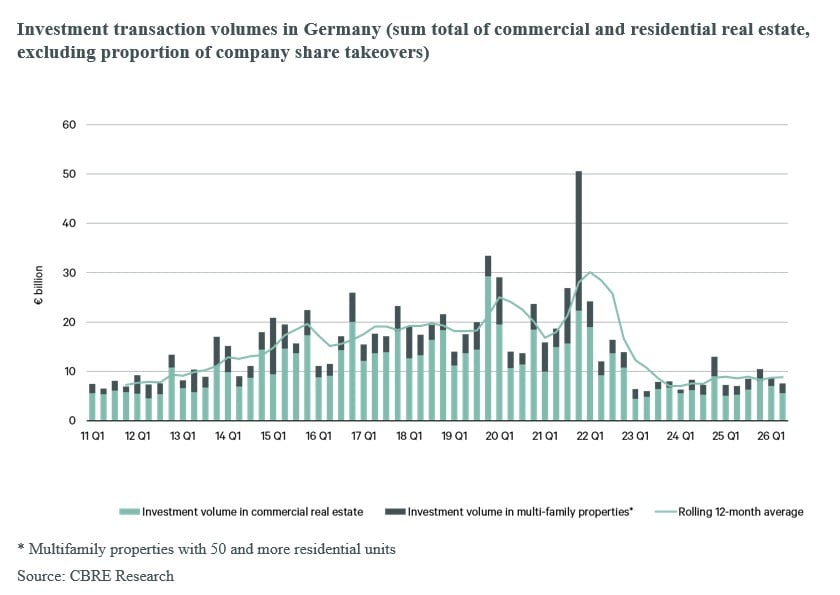

Germany’s real estate transaction volume came in at €16.2 billion in the first half of 2026, reflecting year-on-year growth of 13 percent. Of this volume, almost €13 billion was attributable to commercial real estate, a good one fifth more than in the first half of 2025, so the market is still on track with its gradual recovery. At the same time, transaction activity remained selective, focusing on high quality single-asset transactions and liquid core markets. Momentum in the second quarter slowed a little compared with the start of the year. Geopolitical uncertainties resulted in individual processes being concluded later down the line and led to greater caution around initiating new transactions. This scenario did little to change the market’s fundamental recovery, however. These are the conclusions drawn in a current analysis prepared by the global commercial real estate services company CBRE.

“The gradual recovery is ongoing. We are seeing more activity in the market, more sales processes, and generally more property than a year ago. At the same time, selectiveness is the order of the day on the investment market. Investors continue to concentrate on premium property in liquid markets and go about making their decisions with great discipline. The growing availability of property is a key driver of this trend. This is down to various developments – from imminent refinancings through to the still elevated interest rate level and on to cash outflows from open-ended real estate mutual funds, flanked by institutional investors’ requests for capital repatriation from special funds. This ups the pressure to sell, which ensures additional market activity.”

Marcus Lemli, Head of Capital Markets Germany at CBRE Germany

“The real estate industry fundamentals remain intact and are bolstering Germany’s investment market. At the same time, the pricing process has reached a more advanced stage than a year ago. Germany therefore retains its position as a strategically important target market for international investors. Even if many investors proceed on a very selective basis and domestic capital continues to dominate market activity, there is growing interest.”

Dr. Jan Linsin, Head of Research Germany at CBRE Germany

“The pricing process is a great deal farther down the line than a year ago. Buyers and sellers have gradually aligned their expectations to market conditions. Consequently, the bid-ask spread has narrowed, and transactions are more frequently brought over the line. Concurrently, prime yields in the liquid core markets remain stable for the most part. Outside the prime segment, however, the market is most strongly differentiated by location, property quality and risk profile. Generally speaking, we are seeing a more reliable price level than even a few quarters ago. At the same time, prime yields in some asset classes are showing signs of a slight increase in the second half of the year.”

Sandro Höselbarth, Head of Valuation & Advisory Services Germany at CBRE Germany

Office staging a clear recovery

With an investment volume of €3.45 billion, office real estate increased 66 percent year on year, thereby recording the most substantial revival in the league of large asset classes. The segment benefited from high-profile single-asset transactions in particular. Industrial and logistics properties also picked up momentum and made a significant contribution to boosting the commercial investment market. Conversely, retail suffered a decline. Residential real estate entered a slight downtrend but nevertheless remained the strongest asset class on Germany’s investment markets. Land for development achieved the strongest relative growth, which signifies that investors are prepared to take on greater risk again on a selective basis.

Top 7 markets driving recovery

The seven largest investment locations in Germany that derive benefit from a high level of market liquidity and transparency continued to gain importance in the first half of the year. The Top 7 locations presented a mixed picture. Düsseldorf performed especially well on the back of a few major deals. Cologne, Hamburg and Frankfurt also staged a tangible recovery, as opposed to Berlin and Munich that fell short of their year-earlier levels.

Single-asset transactions determine market activity

As before, the transaction structure was clearly impacted by single-asset transactions in much greater numbers compared with the same period last year, while portfolio transactions trended down slightly. The move toward more granular investment strategies therefore continues to hold sway. At the same time, high-volume transactions achieved greater prominence again: Both the number and the relative proportion of deals over the €100 million mark increased. Around one third of these transactions was accounted for by Berlin, Düsseldorf, Hamburg and Munich. Large-scale single-asset transactions dominated the office segment in particular versus care home and healthcare real estate, logistics and multifamily housing segments where portfolios were traded for the most part. Despite the high number of large-scale transactions, the average deal size dropped to a good €20 million. The key factor here was attributable to the simultaneous increase in the number of small and medium-sized single-asset transactions.

Investment strategies are also evidencing a change. The proportion of core products dropped slightly as more core-plus investments were made. Opportunistic strategies also picked up momentum, as opposed to the value-add segment where development was somewhat weaker. All in all, the market has therefore moved away from a mainly defensive strategy in the direction of more discerning risk positioning.

In terms of buyers, real estate companies, the public sector, along with asset and fund managers proved to be most active market participants. On the seller side, developers, listed real estate companies and REITs took the lead. Accordingly, well-capitalized investors increasingly took advantage of market opportunities while, on the supply side, liquidity-motivated owners brought additional properties to the market. Although international investors stepped up activities, market activity was principally underpinned by domestic capital, the share of which grew further in a year-on-year comparison.

Outlook for the remainder of the year

“We expect the gradual recovery to hold steady in the second half of the year, especially as the pipeline is well filled. A transaction volume of a good €35 billion appears possible for the full year. Although due diligence and decision processes remain challenging and take longer, this will nevertheless filter through in the form of more informed investment decisions and greater predictability regarding transactions. Against this backdrop, the market remains selective with a clear focus on premium property, liquid core markets, and sustainable cash flows” Lemli states.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services. The company has more than 155,000 employees serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, critical infrastructure); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.