Press Release

Residential costs continue to rise – also driven by service charges

07 May 2026

Media Contact

Ass. Director|Communications

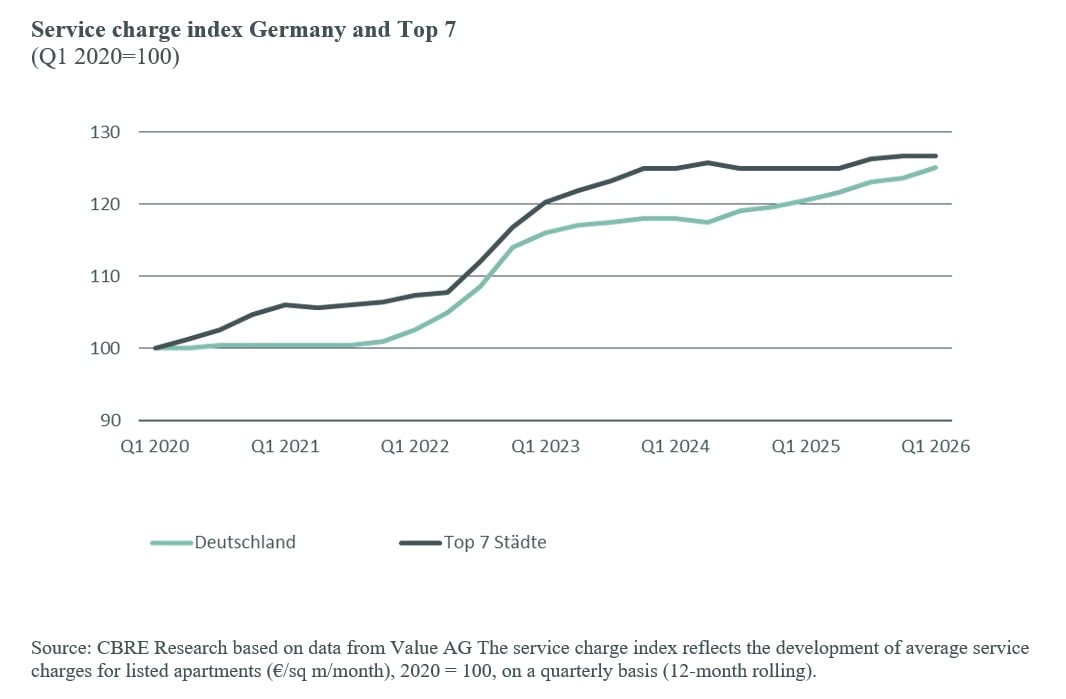

Service charges have also gained increasing importance. Although the sharp rise seen between 2021 and 2023 has recently eased, the overall level remains high. In the first quarter of 2026, average service charges across Germany amounted to €2.49/sq m/month, representing an increase of 3.8% over twelve months. In the Top 7 cities, the cost level was significantly higher at €2.94/sq m. Munich recorded the highest level, reaching €3.47/sq m. The extent of the increase becomes particularly evident over a longer time horizon. Over the past five years, ancillary costs in the Top 20 cities have risen by around 19.5%, almost in line with general inflation (+21.6%). Against the backdrop of the conflict in the Middle East and the resulting disruptions in energy markets, service charges are likely to continue rising. “Service charges are increasingly moving into focus, as they account for a growing share of total housing costs,” says Michael Schlatterer, Managing Director Residential Valuation at CBRE.

“Noticeable relief in the rental housing market is not expected in the short term. Service charges are also likely to remain structurally high despite interim stabilisation, given ongoing geopolitical risks,” says Jirka Stachen, Head of Research Consulting Continental Europe at CBRE.

The period of declining asking prices for owner-occupied apartments has also come to an end. Prices have largely stabilised across the Top 20 markets and are rising again in selected cities. The average median asking price in the first quarter of 2026 stood at around €4,200/sq m, approximately 3% above the previous year’s level. The strongest price increases were recorded in Essen, Bonn and Dresden.

Investment market remains constrained amid limited supply

Structural scarcity continues in the professional investment market. Despite slightly rising building permits, high construction costs and restrictive financing conditions are preventing any material expansion of housing supply. In many major cities, vacancy rates in marketable multi-family housing remain below 2%. “At the same time, the market continues to be characterised by a certain degree of restraint, primarily due to high financing costs and divergent price expectations between buyers and sellers, which led to a decline in transaction volumes in the first quarter,” says Stefan Wilke, Head of Residential Investment Germany at CBRE. “Nevertheless, we are seeing investors becoming more active again, reviewing opportunities more closely and positioning themselves selectively.”

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services. The company has more than 155,000 employees serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, critical infrastructure); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.