Press Release

Retail real estate investment market ticks up in 2025

13 January 2026

Media Contact

Bettina Bierhalter

Ass. Director|Communications

- Investment volume up two percent to €6.4 billion year on year

- Twelve transactions above the €100-million mark

- Very little movement in prime yields

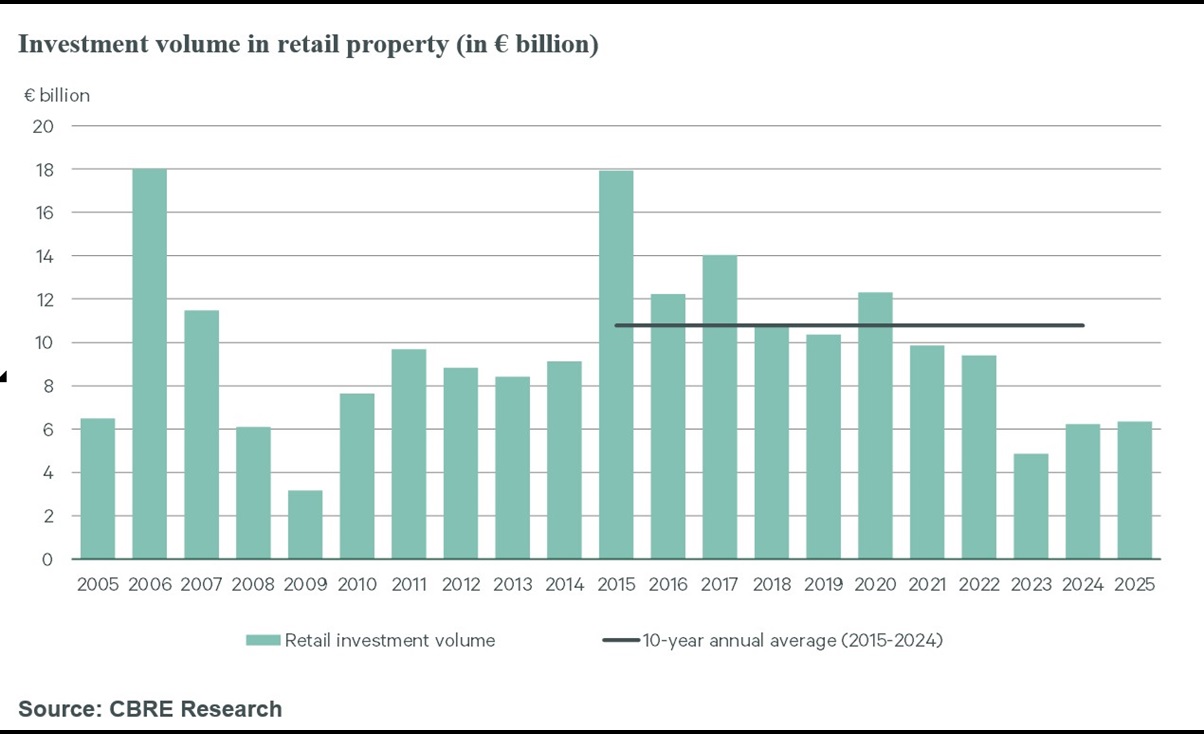

Germany’s retail real estate investment market delivered a transaction volume of €6.4 billion in 2025, marking growth of two percent year on year. Since 2021 the share of retail properties in the commercial real estate investment market has risen steadily to currently 26 percent, which puts this asset class in second place (behind logistics and ahead of office). One reason for the recent increase is to be found in the twelve large-scale transactions over the course of 2025, each of more than €100 million. Among other deals, the Porta-Portfolio takeover by XXXLutz, the disposal of Oberpollinger in Munich, the sale of the Designer Outlets in Neumünster and near Berlin, as well as the Gropius Passagen in Berlin and several grocery-anchored real estate portfolios figured as the most prominent transactions in this segment. This is the conclusion drawn in an analysis prepared by the global commercial real estate services company CBRE.

“The investment market’s confidence in the asset class of retail continued to grow in 2025. Various large-scale transactions took place, including portfolios, with perceptible new activity on the part of international investors.”

Jan Schönherr, Head of Retail Investment at CBRE Germany

The share of portfolios climbed 13 percentage points to 31 percent. The proportion of international investors advanced six percentage points to 45 percent.

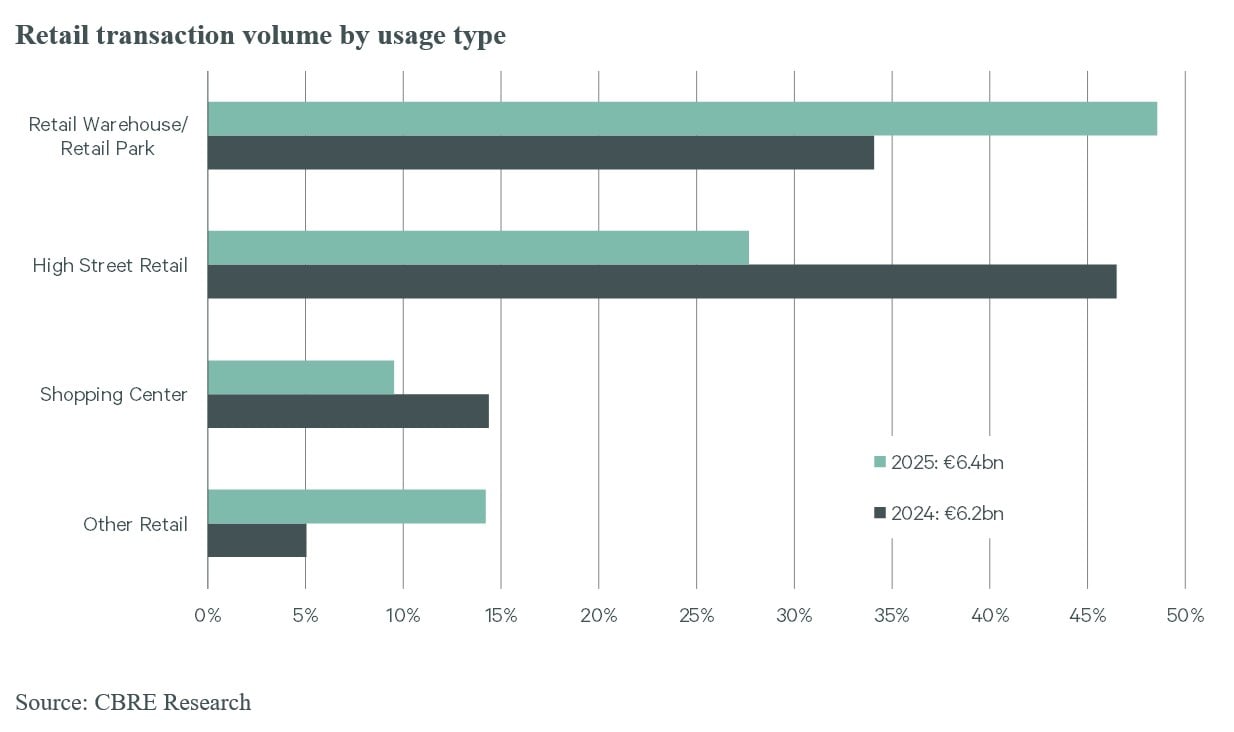

Retail warehouses and retail parks emerged as the strongest segment in 2025, together accounting for a share of 49 percent (up 15 percentage points) in the retail real estate investment market. They were followed by high street properties with 28 percent (down 20 percentage points) and shopping centers with 10 percent (down four percentage points). The group of retail park and retail warehouse properties have therefore regained their traditional status as the strongest segment within the retail real estate investment market, while high street properties that dominated the previous year of 2024 still captured a market share that exceeded the long-term average.

“Prime yields remained relatively stable in 2025”, says Anne Gimpel, Team Leader Valuation Advisory Services at CBRE Germany. In the final quarter, only shopping centers in secondary locations showed a change in prime yield that increased by 0.25 percentage points to 7.75 percent. By contrast, other segments saw smaller declines in achievable prime yields compared with the year-earlier period. Declines in these dimensions were sustained by high street properties in the Top 7 markets (down 0.2 percentage points to 4.44 percent), food markets (down 0.1 percentage points to 4.6 percent), as well as retail parks (down 0.1 percentage points to 4.9 percent). Conversely, shopping centers in prime locations remained stable at 5.9 percent.

Outlook for 2026

“Given a well-filled deal pipeline, it is looking like a brisk start to the year following a good year-end quarter. Demand is also holding steady, especially for grocery-anchored properties and properties ininner-city locations We are therefore assuming a transaction volume of around six to seven billion euros again in 2026,” Schönherr says in anticipation. “We are registering interest from international players with good liquidity and a focus on value-add and core plus who are screening the German market for retail properties.”

“There are also no signs so far of changes in yield levels in the short term either,” Gimpel adds.

- Twelve transactions above the €100-million mark

- Very little movement in prime yields

Germany’s retail real estate investment market delivered a transaction volume of €6.4 billion in 2025, marking growth of two percent year on year. Since 2021 the share of retail properties in the commercial real estate investment market has risen steadily to currently 26 percent, which puts this asset class in second place (behind logistics and ahead of office). One reason for the recent increase is to be found in the twelve large-scale transactions over the course of 2025, each of more than €100 million. Among other deals, the Porta-Portfolio takeover by XXXLutz, the disposal of Oberpollinger in Munich, the sale of the Designer Outlets in Neumünster and near Berlin, as well as the Gropius Passagen in Berlin and several grocery-anchored real estate portfolios figured as the most prominent transactions in this segment. This is the conclusion drawn in an analysis prepared by the global commercial real estate services company CBRE.

“The investment market’s confidence in the asset class of retail continued to grow in 2025. Various large-scale transactions took place, including portfolios, with perceptible new activity on the part of international investors.”

Jan Schönherr, Head of Retail Investment at CBRE Germany

The share of portfolios climbed 13 percentage points to 31 percent. The proportion of international investors advanced six percentage points to 45 percent.

Retail warehouses and retail parks emerged as the strongest segment in 2025, together accounting for a share of 49 percent (up 15 percentage points) in the retail real estate investment market. They were followed by high street properties with 28 percent (down 20 percentage points) and shopping centers with 10 percent (down four percentage points). The group of retail park and retail warehouse properties have therefore regained their traditional status as the strongest segment within the retail real estate investment market, while high street properties that dominated the previous year of 2024 still captured a market share that exceeded the long-term average.

“Prime yields remained relatively stable in 2025”, says Anne Gimpel, Team Leader Valuation Advisory Services at CBRE Germany. In the final quarter, only shopping centers in secondary locations showed a change in prime yield that increased by 0.25 percentage points to 7.75 percent. By contrast, other segments saw smaller declines in achievable prime yields compared with the year-earlier period. Declines in these dimensions were sustained by high street properties in the Top 7 markets (down 0.2 percentage points to 4.44 percent), food markets (down 0.1 percentage points to 4.6 percent), as well as retail parks (down 0.1 percentage points to 4.9 percent). Conversely, shopping centers in prime locations remained stable at 5.9 percent.

Outlook for 2026

“Given a well-filled deal pipeline, it is looking like a brisk start to the year following a good year-end quarter. Demand is also holding steady, especially for grocery-anchored properties and properties ininner-city locations We are therefore assuming a transaction volume of around six to seven billion euros again in 2026,” Schönherr says in anticipation. “We are registering interest from international players with good liquidity and a focus on value-add and core plus who are screening the German market for retail properties.”

“There are also no signs so far of changes in yield levels in the short term either,” Gimpel adds.

About CBRE Group, Inc

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services (based on 2025 revenue). The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, data center solutions); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services (based on 2025 revenue). The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, data center solutions); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.